Navigating the mortgage landscape in the Upper West Side of New York City can be a complex endeavor, given the area's unique real estate market and diverse range of property types. With its historic brownstones, luxury condos, and co-op apartments, the Upper West Side presents a variety of options for prospective buyers. Understanding the intricacies of mortgage options is crucial for making informed decisions and securing the best possible terms for your investment. This exploration of mortgage options will provide valuable insights into the factors that influence mortgage choices and the steps to take when purchasing a home in this iconic neighborhood.

Understanding Mortgage Types

The first step in navigating mortgage options is understanding the different types available. In the Upper West Side, buyers can choose from conventional loans, jumbo loans, and government-backed loans such as FHA or VA loans. Conventional loans are popular for those with good credit and a substantial down payment. Jumbo loans cater to properties that exceed the conforming loan limits, which is common in high-value areas like the Upper West Side. Government-backed loans, while less common in this affluent neighborhood, can be an option for those who qualify. Each mortgage type has its own set of requirements and benefits, making it essential to evaluate which aligns best with your financial situation and home-buying goals.

Evaluating Interest Rates and Terms

Interest rates and loan terms are critical factors in determining the overall cost of a mortgage. Fixed-rate mortgages offer stability with consistent monthly payments, while adjustable-rate mortgages (ARMs) may start with lower rates that can change over time. In the Upper West Side, where property values are high, even small differences in interest rates can significantly impact the total cost of a loan. It's important to compare offers from multiple lenders to find the most favorable rates and terms. Additionally, understanding the implications of different loan terms, such as 15-year versus 30-year mortgages, will help buyers make informed decisions that align with their long-term financial plans.

Assessing Down Payment Requirements

Down payment requirements can vary widely depending on the type of mortgage and the lender. In the Upper West Side, where property prices are often substantial, a larger down payment can be advantageous. It can reduce the loan amount, potentially lower interest rates, and eliminate the need for private mortgage insurance (PMI). Buyers should assess their financial situation to determine how much they can comfortably allocate for a down payment. It's also wise to consider the impact of the down payment on liquidity and other investment opportunities.

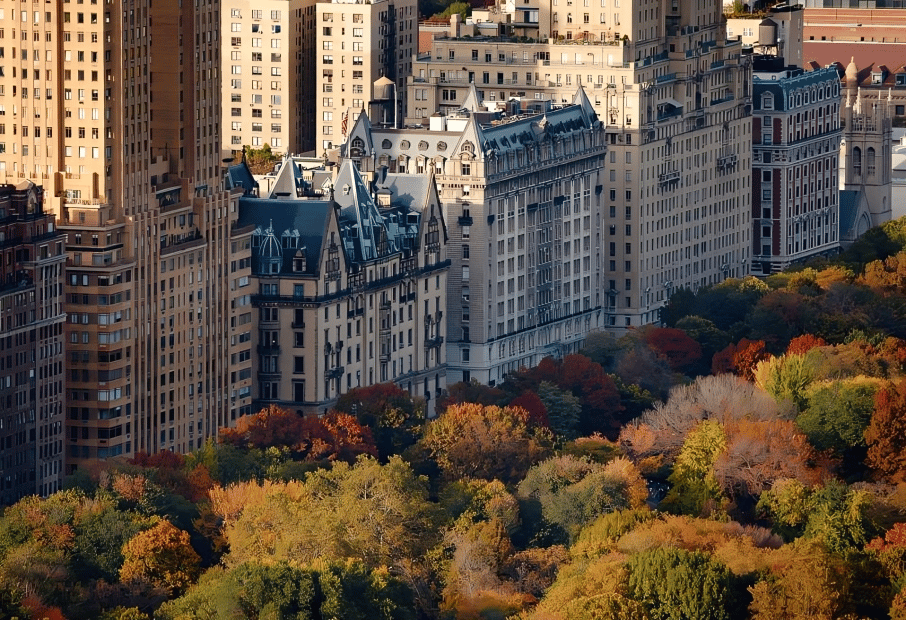

Navigating Co-op and Condo Financing

The Upper West Side is known for its co-op and condo properties, each with distinct financing considerations. Co-op purchases often require board approval and may have stricter financial criteria, including higher down payments and post-closing liquidity requirements. Condo financing, on the other hand, is typically more straightforward but may include additional assessments or fees. Understanding the specific requirements and nuances of financing these property types is crucial for buyers. Working with a real estate agent familiar with Upper West Side properties can provide valuable guidance in navigating these complexities.

Exploring Pre-Approval and Pre-Qualification

Securing pre-approval or pre-qualification is an important step in the home-buying process. Pre-qualification provides an estimate of how much a buyer might be able to borrow, while pre-approval involves a more thorough evaluation of financial information and creditworthiness. In a competitive market like the Upper West Side, having a pre-approval letter can strengthen a buyer's offer and demonstrate serious intent to sellers. It's advisable to gather necessary documentation, such as income statements and credit reports, to streamline the pre-approval process.

Considering Closing Costs and Fees

Closing costs and fees are additional expenses that buyers need to account for when purchasing a property. These can include appraisal fees, attorney fees, and title insurance, among others. In the Upper West Side, where real estate transactions can be complex, understanding and budgeting for these costs is essential. Buyers should request a detailed estimate of closing costs from their lender and factor these into their overall financial planning. Being prepared for these expenses can prevent last-minute surprises and ensure a smoother closing process.

Working with a Knowledgeable Real Estate Agent

Partnering with a knowledgeable real estate agent who specializes in the Upper West Side can be invaluable. An experienced agent can provide insights into the local market, recommend reputable lenders, and assist with navigating the intricacies of co-op and condo purchases. They can also help buyers identify properties that meet their criteria and negotiate favorable terms. Choosing an agent with a strong track record in the Upper West Side can enhance the home-buying experience and increase the likelihood of a successful transaction.

Understanding the Impact of Credit Scores

Credit scores play a significant role in determining mortgage eligibility and interest rates. In the Upper West Side, where property values are high, maintaining a strong credit score can lead to more favorable loan terms and lower interest rates. Buyers should review their credit reports for accuracy and address any issues before applying for a mortgage. Paying down existing debt, avoiding new credit inquiries, and making timely payments can help improve credit scores and enhance mortgage options.

Evaluating Lender Options

Choosing the right lender is a crucial step in the mortgage process. Buyers in the Upper West Side have access to a variety of lenders, including banks, credit unions, and mortgage brokers. Each lender may offer different rates, terms, and service levels. It's important to compare multiple lenders to find the best fit for your needs. Consider factors such as customer service, responsiveness, and the ability to close on time. Building a relationship with a lender who understands the Upper West Side market can provide additional support throughout the home-buying journey.

Planning for Future Financial Goals

When selecting a mortgage, it's important to consider how it aligns with future financial goals. Buyers should evaluate their long-term plans, such as potential career changes, family growth, or investment opportunities. The Upper West Side's dynamic real estate market can offer both challenges and opportunities, making it essential to choose a mortgage that provides flexibility and supports overall financial objectives. Consulting with a financial advisor can help buyers assess their options and make informed decisions that align with their broader financial strategy.

Ready to Find Your Dream Home?

Navigating mortgage options in the Upper West Side can be a complex journey, but with the right guidance, it becomes much more manageable. By understanding your options and working with knowledgeable professionals, you can secure a mortgage that fits your needs. If you're ready to take the next step in finding your dream home, Chana Ofek is here to help. Contact Chana today to explore the best mortgage options for your new Upper West Side home.